“People think good decision-making is about being right all the time. It’s not. It’s about lowering the cost of being wrong and changing your mind.” – Shane Parrish, Farnam Street

Required reading for what follows:

- My initial Twitter thread on selling Minera Alamos after the deal was announced Thursday.

- The investor presentation MAI put together explaining the deal.

- Incoming chairman Jason Kosec’s interview with the KE report explaining why he got involved with the company.

The pre-amble

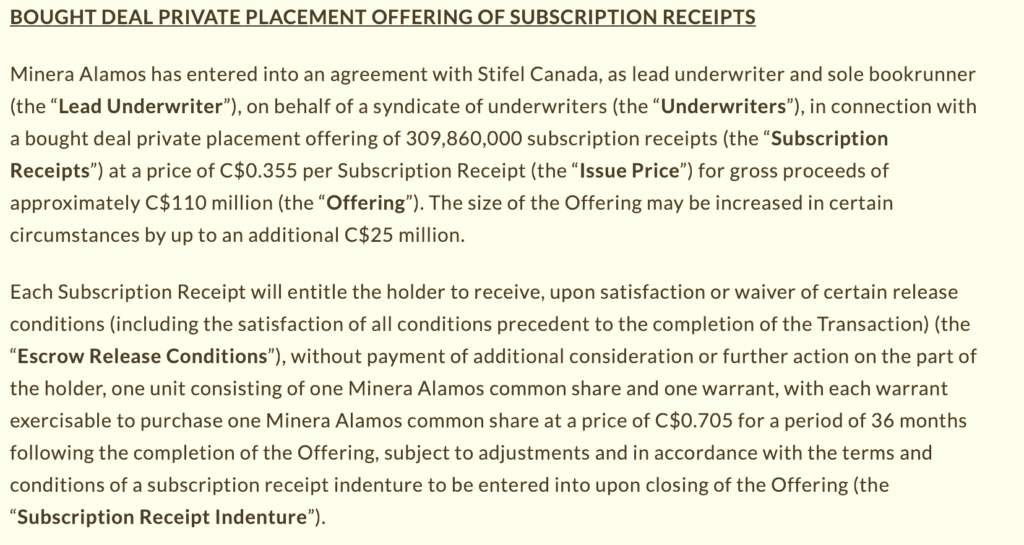

I’m not going to call it an acquisition as that’s not really accurate given the 80% dilution of existing shareholders. But for those that aren’t already aware, Minera Alamos is getting restructured. Along with a new chairman in Jason Kosec, MAI absorbs the producing Pan mine in Nevada, along with the Gold Rock and Illipah development projects, from Equinox Gold. Minera Alamos also gets new institutional shareholders from Kosec’s network who will be financing the bulk of the purchase. Those new MAI shareholders are getting a deal.

The cost

The transaction torches the current share structure and previous management ethos of avoiding dilution, etc. The investor presentation doesn’t go into the post-acquisition share structure. Here are the back of the napkin numbers.

- MAI shares outstanding: 577.4-million

- MAI shares issued to Equinox: 97-million

- Shares issued to new Kosec investors in the fully subscribed financing: 380-million

- Net debt payable after making some adjustments: $16.4-million

Warrants and options

- Management options: 27.7-million (avg. exercise price 40 cents)

- Warrants issued to new Kosec investors in the financing: 380-million (36 month term and 70.5 cent strike)

Why I sold

Equinox is not in the business of owning junior miners and will sell those shares as soon as possible. And with more than a billion shares outstanding pro-forma, there’s a huge warrant overhang that puts a cap on the share price. Shareholders are facing another 40% dilution if things actually go well – and if they don’t it means the share price will remain below 70 cents for the next three years. Permits for Santana or Cerro De Oro would have caused the shares to rally – and I thought that would have allowed MAI to finance at better terms with the optionality of moving forward with construction of Copperstone. With a pivot this big, the company disagreed and the finances at MAI were clearly worse than I thought. The financing terms suggest desperation.

Copperstone wasn’t the most important asset inside Minera Alamos but until Thursday it was the fulcrum asset. Putting it into construction would validate the company’s value proposition as efficient mine builders and provide cash to realize the Mexican asset value once permits arrive (I still believe they will arrive). Pan has now become that fulcrum asset.

This is a small mine producing 35-40 thousand ounces a year, but after talking to people with Nevada experience this weekend I believe Pan is at the end of its life with minimal exploration potential. Management says it can increase production at Pan, but this isn’t a management team with a lot of credibility at the moment.

Given the risk of Equinox selling pressure, another financing if Pan can’t pay all the bills, and the need for something monumental to happen for MAI shares to break through the 70-cent ceiling from the warrant overhang, Minera Alamos is a clear sell.

However restructurings – and this is absolutely a restructuring – can deliver big returns to patient, contrarian investors. I’ll be talking to new chairman Jason Kosec later today to see if he can change my mind on any of the above.

Adding to Star Royalties

I wasn’t planning to add to Star Royalties, but the I picked up more shares below 23 cents, slightly raising my cost base. Star owns a 4% life-of-mine stream on Copperstone and 9.6-million shares of Minera Alamos. Those MAI shares are obviously less valuable today than they were last week, but the credibility of Minera Alamos now rests on increasing production at Pan and getting Copperstone into production next year without coming back to the market for more money. The new MAI presentation says Copperstone will be producing by the fourth quarter of next year, which is only a few months later than I was expecting.

Copperstone is a more valuable asset today but one that won’t be in production for at least another year. Consolidation has arrived in the royalty space. I’d urge CEO Alex Pernin and the Star management team to sell the mining royalty portfolio and dividend out the Minera Alamos shares to Star shareholders. Start the process of winding down this failed holding company and surfacing the asset value for shareholders. I’m moving Star from the royalty section of the portfolio to the specials/workouts section to reflect my opinion it should be liquidated, and soon.